Preliminaries

While we can’t fix the flawed concept of getting more for less or the un-American concept of taking from one group for the benefit of another without asking, we can point out the massively fatal conception of a single portal at HHS to display plans and pricing from various healthcare insurance providers, collect sensitive income tax information, and interface with a plethora of other websites, including IRS and individual insurance providers.

We also cannot put too fine a point on violation of the 10th Amendment by allowing the Federal government to dictate what voluntarily happens solely inside a state with regard to healthcare insurance (or anything else). The Supreme Court has reviewed to some extent the appropriateness of PP&ACA penetrating a state’s sovereignty over business wholly contained within its borders, and to some extent has reviewed the constitutionality of imposing a “tax” for failing to purchase a compliant policy and to a minor extent the constitutionality of granting a tax subsidy to some Americans over others (relying in large measure on the 16th Amendment).

Website Functionality

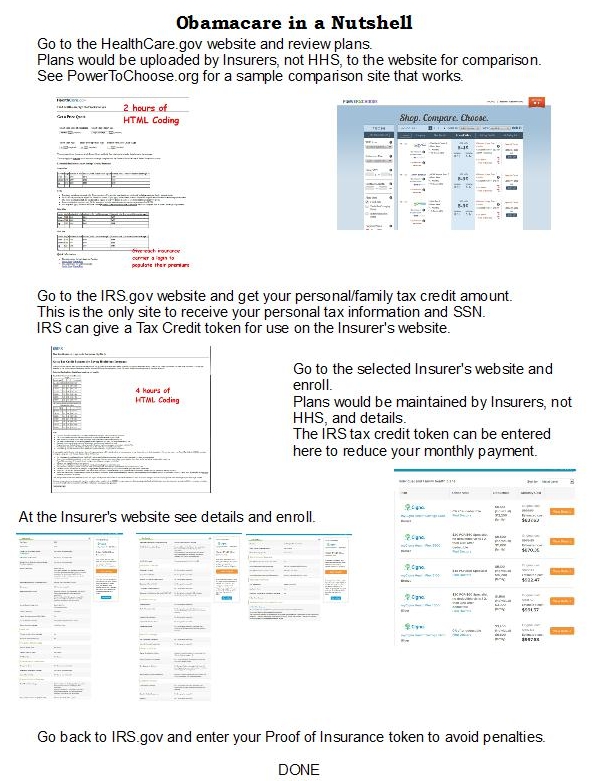

Supposing for a moment that PP&ACA is fully constitutional (which it most assuredly is not), implementing it is so simple as to baffle any web person anywhere as to why the government spent several $100s of millions of dollars on programming to attempt to make a website portal for it.

- Central Point to Define Goals & Objectives of PP&ACA

- Information about Key Provisions of the law

- Central Point of Offerings from All Insurers

- Jumping Off Point to Insurance Providers to Enroll in a Plan

- Jumping Off Point to IRS to Verify Tax Credits and Arrange for Payment

Insurance Providers currently operate websites so they need only add some functionality to their websites and to push their policy offerings to the Healthcare.gov website in a standard format.

IRS operates its website and needs only add a method for taxpayers to login or create a login to apply for a tax credit, or report coverage according to PP&ACA.

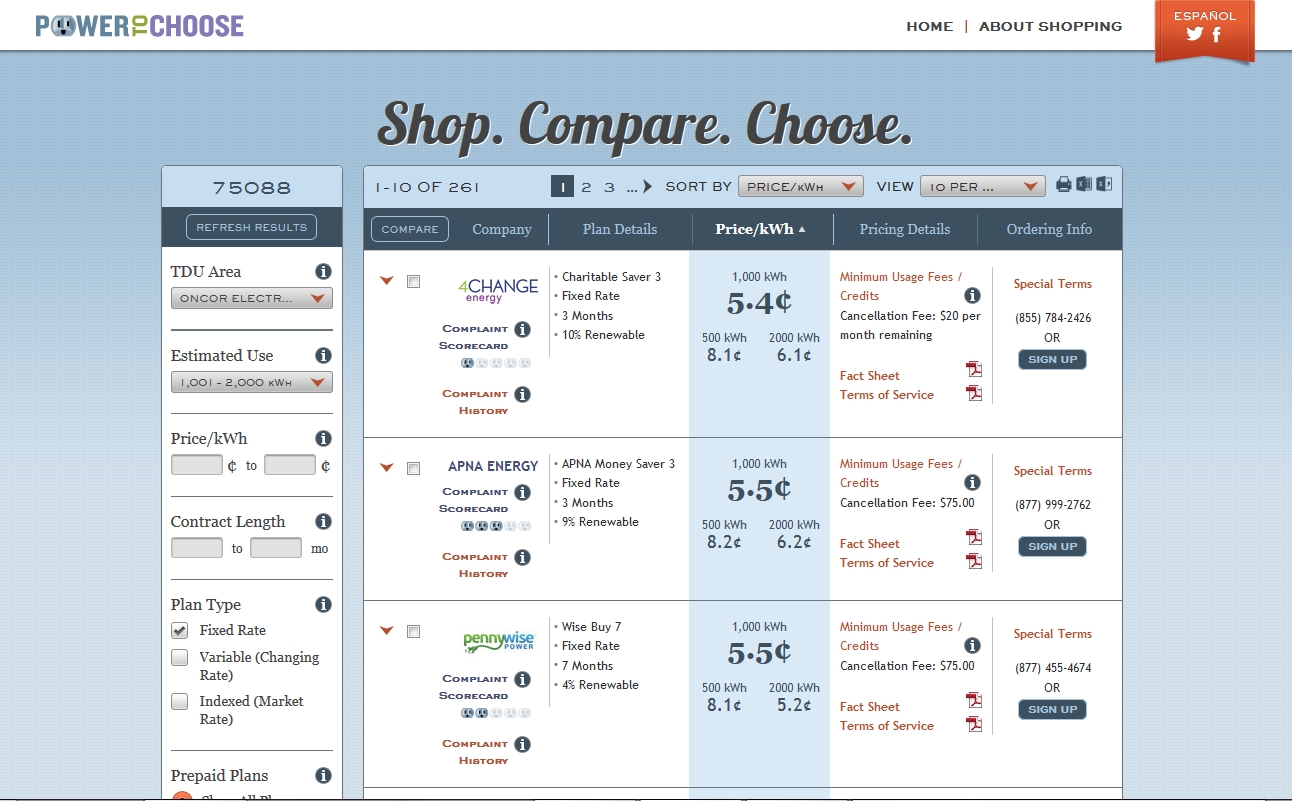

Healthcare.gov needs to add a Marketplace, like the electric provider marketplace PowerToChoose.org. PowerToChoose allows electric providers to create an account and upload electricity plans. Each offering is covered by an Electricity Facts Label, containing standardized language to describe all the features of the offering, including monthly fees, per kW-hr charge, billing charges, taxes and so on. PowerToChoose can sort the display to show only “green” providers, lowest rates, longest terms, monthly charge and so on.

HHS – Healthcare.gov

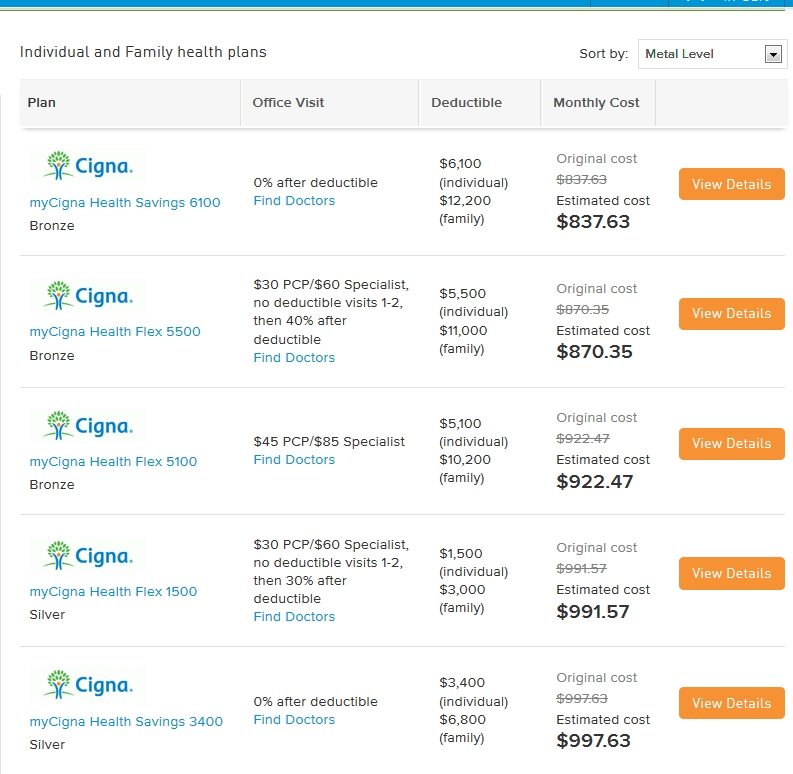

By comparison, Healthcare.gov needs only create a standard “label” for each plan showing what is covered by law (identified as “Bronze” “Silver” etc), family size, deductible, co-pays, and so on. Giving each insurance provider the ability to login and manage their offerings is fairly simple. After populating the offering database, Healthcare.gov needs to add the functionality of sorting by various fields, including price, deductible and so on.

Security is not much of an issue, because only publicly available data is kept by HHS, nothing personal, such as Social Security account numbers and the like. No personal logins are necessary on the HHS website, ever.

Like PowerToChoose each offered product contains a clickable link to the provider. Clicking the link pulls the identified plan over to the provider. The “Insurance Plan Label” can easily be the first thing the user is presented when a user clicks through on the HHS website.

Insurance Provider Website(s)

If the user likes the plan that is pulled up, the user can apply at the provider’s site, just like in the PowerToChoose scenario. Whatever method the insurance provider uses for creating logins remains the same. Security is a responsibility of the provider, not the government. As will be explained momentarily, only a normal login account, as would be found on Amazon or any other on-line merchant, is necessary, because no tax information, no Social Security information or other sensitive information is used by the provider. The insurer is prohibited from asking for the Social Security account number.

If the user likes the plan that is pulled up, the user can apply at the provider’s site, just like in the PowerToChoose scenario. Whatever method the insurance provider uses for creating logins remains the same. Security is a responsibility of the provider, not the government. As will be explained momentarily, only a normal login account, as would be found on Amazon or any other on-line merchant, is necessary, because no tax information, no Social Security information or other sensitive information is used by the provider. The insurer is prohibited from asking for the Social Security account number.

Payment is somewhat more complicated because of the tax credit issue, which we will deal with shortly.

IRS – Tax Credits

Currently a user can create a login at IRS but the purpose of that needs to include applying for a tax credit and to report compliance with the PP&ACA requirement for purchasing.

The second thing first, employers can report compliance for employees by reporting coverage in an employer’s healthcare plan. Individuals can report coverage using a login account. Users will receive a Proof of Insurance token from their provider. The user logs in, selects the name of the provider, and enters the token provided by the insurance provider. Simple.

The first thing is the tax credit and a similar Tax Credit Authorization token will be issued by IRS once the user enters the relevant information. Employers will also be able to get the token, if one is authorized. An authorization may be used with the insurance provider to apply the tax credit directly to bills.

Individual Users log into IRS after creating a login account using full legal name (as on W-2), address of residence, Social Security Number and establishing a password. Joint filers can create a separate login for spouse with a separate password, which either can manage, including bifurcation of login accounts and the tax credits themselves.

Employers can create a login account plus additional logins for managing any employees’ accounts; in addition employees can create login accounts to view their accounts but cannot make changes unless authorized by a managing account. Married employees may create a spouse login to view all employers of each other, but with change access

Employers can create a login account plus additional logins for managing any employees’ accounts; in addition employees can create login accounts to view their accounts but cannot make changes unless authorized by a managing account. Married employees may create a spouse login to view all employers of each other, but with change access

Insurance Provider Website

Back on the Insurance provider’s website the user (or employer) enters the tax credit authorization token for the insured. The insurance provider can then verify the authenticity of the token by logging into the IRS website as a provider of insurance and submitting the token with the insured’s name and date of birth. If valid, IRS will in turn authorize payment to the insurer from Treasury. The token is normally issued with no expiration and whichever insurance provider submits the token first will be paid by month-end. If the token is submitted by more than one insurer, then the second insurer to submit it will be rejected, but if payment to the first insurer has not yet been paid, the payment will be suspended and a notice sent to you by Treasury. You must then return to the IRS and get a new Tax Credit Authorization token and give it only to the insurer you want to use.

Universal Service Fund (USF) – More Flawed Thinking

In 1997 Congress passed into law a supplemental fee tacked onto telephone bills. The fund was intended to be used to pay for service for the indigent, usually elderly or just poor, to supply a simple, black dial telephone landline at very low or no cost. That fund is now being tapped to supply smartphones with web browsers to anyone who claims to be poor.

Universal Medical Care may be a noble objective, and no one can belittle the objective. However, the abuse of the USF for webphones should give pause to anyone desiring the same type of “free” medical care. Any program that lends itself to abuse like USF should be viewed suspiciously. Taking from some citizens without authorization from them individually to pay for a thing for others to use is just a form of wealth re-distribution. Re-distributing wealth is a goal many Socialists and Communists have, but it rails against the fundamental concepts embodied in our Constitution.

The 10th Amendment reserves to States and to the people, respectively, all powers not specifically granted to the Federal government within the Constitution. While SCOTUS did enable the PP&ACA to go forward, the question of whether states can maintain the healthcare insurance plans offered wholly within their own states should be decided. Congress can under the Commerce clause in Section 8 regulate interstate insurance policies of all kinds, but there simply weren’t any such policies until now.

Admittedly, the 16th Amendment was a decades-long battle the greedy Socialists won, allowing the Federal government to tax the individuals differently within a State and differently between States. The original concept of the Federal government receiving funds from States, not individuals, in proportion to population. These were alternatively called Direct Taxes. The philosophy was that rich and poor would not be taxed differently. Communists introduced the phrase “to each according to need, from each according to their ability [to pay]”. The 16th Amendment enabled this Communist thinking to be implemented.

Ample evidence exists, especially after the fall of the Berlin Wall, that Communism destroys incentives necessary to make our economic system work. While flaws may exist, such as not recouping costs unfairly imposed on others, in our economic system, we should be addressing those problems rather than attempting to make a failed philosophy work. So many times retirees and investors have been cheated, but when law enforcement stepped in to correct the problem, they seized the booty and refused to compensate the victims. Fines often do nothing for victims. Reparations for damages often go to line the pockets of those in the system, rather than those afflicted by unlawful, unethical acts.

Fatally Flawed Concepts

The entire purpose of the PP&ACA was to protect insureds and provide low-cost insurance coverage for healthcare. First, the cost of healthcare is not addressed by addressing only the cost of insurance coverage. If anyone studied the cost drivers of healthcare, we simply don’t know what they found. Some say it’s the litigation costs, some say it’s the unnecessary testing and procedures, some say it’s the lack of supply of medical professionals, and some say it’s the required overhead of paperwork for insurance claims themselves. Without doctors, hospitals and other healthcare professionals speaking up about why it costs so much per person to provide healthcare, we cannot address the fundamental drivers of those costs. PP&ACA does not address the costs, just payments and insurance coverage. This short-sighted approach is doomed to fail.

Second, we have witnessed on TV the character who can analyze and diagnose any patient condition. Dr House doesn’t really exist, but there are thousands of fine doctors and practitioners who could readily emulate him. In addition, IBM built a futuristic machine that competed on another TV show Jeopardy! The machine, Watson, won the match with two human contestants. Artificial Intelligence (AI) will eventually be introduced into healthcare in a major way. Not only in the diagnosis process but also the treatment process AI can reduce the time it takes and reduce risks of drug interactions and improve surgical procedures via more robotic approaches. Risk reduction, improved diagnosis and treatment are all factors that reduce costs.

Third, the two provisions in the law of no-drop (prohibition against policy cancellations) and no-limit may seem fair, but only the no-drop seems feasible. The no-limit provision will eventually come back to haunt us all. If a life must be preserved at all costs without limit, then someone has to foot that bill. No one wants to give up on a loved one, a child, a parent, a spouse. How can we say not to take extraordinary measures to keep them alive? Of course, we’ll insist on doctors doing “everything” possible. The only limitation will be that imposed by the patient, perhaps by living will. It is likely that a contest will take place among family members to see who can authorize more treatments, proving their greater love of the patient. Where does that end?

If the patient is comatose, it never ends. The no-limit provision is absurd on the face of it. At some point in the future others will realize this and push to impose common-sense limits in place of the no-limit policy. One reason many fear PP&ACA is the likelihood of “death panels” or independent treatment review boards who will impose limits, not by cost, but rather by fiat of “best practices” in healthcare. If you as guardian for the patient decide after discussing with physicians that a treatment is warranted, this decision should override what “best practices” dictate, but it is unlikely that guardians or patients can override such external fiats. At first, of course, no limits will apply, but as the healthcare system is bogged down with hundreds of thousands of extraordinary treatments being applied, IPAB will kick in because of the exorbitant costs involved.

The difficulty of substituting a limit is the same difficulty faced by all collective decisions: my opinion, your opinion and the opinion of everybody else are going to conflict. Is a life worth $43M in procedures? $10M? $1M? Who decides that? Will we vote on it? Will HHS decide when the $5T HHS healthcare spending limit is reached? How much effort and who will decide on best practices is a looming problem. At least the no-drop provision is less damning. While annual and lifetime limits have been the norm for decades. As painful as they have been, we may need to keep one or both of them going forward. In a socialized economy we will have to vote on what that or those limits actually are.

Fourth, the regulation of interstate commerce is valid, but invalidating healthcare insurance policies that are offered solely within a state by a state-domiciled insurance provider was wrong to begin with. Grandfathering of existing policies that do not cross state borders is crucial.

Fifth, employers faced with penalties for not covering their workforce when it exceeds 50 employees will likely weigh the cost of providing insurance coverage versus paying the penalty and elect to pay the penalty, resulting in loss of coverage for those employees. Worse, employers may elect to reduce the hours of employees so that they are not counted as part of their workforce to under 30 hours per week. Those employees with only part-time employment will lose their coverage under existing plans. Both of these possible outcomes are unintended consequences and should be avoided. How? As long as the employer mandate is in place, the consequences cannot be avoided. The employer mandate must be eliminated.

Why is 50 the magic number at which an employer suddenly becomes responsible for providing a group policy? Why not 1,000 or 10,000? Why not 10? Only 10, you say, would mean adding a whole person just to manage the program without any offsetting benefit, like increased sales or reduced costs, for the employer. But the same can be said of 50 employees (2% of employees). Maybe around 250 employees (1/4% of employees) it becomes feasible without severely affecting the bottom line.

Reasoning should tell us that group insurance is a benefit created 7 decades ago when FDR imposed price controls and wage controls to keep the war economy from overheating. The employers competed with each other in a sort of non-wage benefit. It was not and should not be looked upon as an employer responsibility to offer healthcare or any other type of insurance. If employers want to compete with each other by offering insurance programs, let them; but how can we by law decide that 50 is the correct number to impose a mandatory insurance program? Why not 25 or 100? What makes it rational or a business imperative to choose 50? It cannot be justified and needs to be withdrawn.

Lastly, fairness demands that whatever the cook brings out of the kitchen everyone has to eat. The cook can’t make himself something special and serve swill to the masses. If it’s good enough for the public, then it’s good enough for public officials, too. PP&ACA should apply to the entire collective, including George Soros and Warren Buffett besides the President and all Federal officials alike. No exceptions, no exemptions, period.

Besides all these points, there are alternatives we can entertain in another article.